By Katherine Adkins, Chief Legal Officer, Affirm

Consumer spending is the engine that drives the American economy, accounting for roughly 70% of U.S. GDP by most estimates. If spending is the engine, then access to credit is the fuel. For over a decade, Affirm has been committed to responsibly extending access to credit and to make payments more transparent, efficient, and consumer-friendly.

Like other new and disruptive industries, we understand that there are always going to be questions to answer and skepticism to address. But, we actually welcome debate and dialogue, especially when it is well-informed and anchored in what is best for consumers.

Recently, the Consumer Financial Protection Bureau (CFPB) released a new report on ‘Buy Now, Pay Later’ (BNPL). While the more recent report represents an admirable attempt to provide additional insights into how consumers are using pay-over-time options, it also could not delve into important nuances and distinctions given the anonymized nature of aggregating data from across the industry. As a senior leader at Affirm, the leading pay-over-time provider, I felt compelled to provide some of this crucial additional context to help paint a more accurate, and complete picture – at least from the Affirm side. After all, we are a bunch of geeks that love numbers and outlining the importance of what we do in pursuit of our mission to deliver honest financial products that improve lives.

Understanding the research’s methodological limitations

The CFPB claims this research will “fill the data gap” of the BNPL sector. For its part, Affirm is committed to greater industry transparency and helping close that gap – as a publicly traded company, Affirm discloses a significant amount of information about our business and we also already furnish some monthly loans, which make up a majority of our volume, for credit reporting.

Unfortunately, despite the CFPB’s aims, the research has a number of limitations. The CFPB analysis relies on data from 2020-2022. BNPL is still a relatively young, dynamic sector that experienced incredible growth and change during that period – not to mention since. It would be prudent to look at conclusions from dated statistics with several grains of salt.

But more importantly – and why I ultimately decided to jot down these thoughts – is that the report aggregates information from six fundamentally different companies to make broad generalizations about an industry and population. This overly broad brush characterizes an entire industry and consumer population as homogenous, obscuring critical differences, for example, in business models and underwriting practices, which can lead to very different consumer outcomes.

Who really uses BNPL

While the CFPB report suggests that borrowers with subprime or deep subprime credit scores make up the majority of BNPL originations across the industry, it's important to note that this isn't representative of all providers.

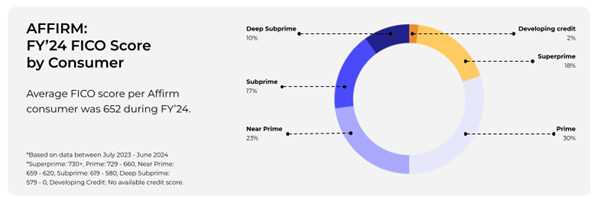

Nearly three-quarters (71%) of Affirm’s consumer base are near prime, prime or superprime compared to just 35% among the aggregated figures in the CFPB’s report (see the graphic below). These represent borrowers with FICO scores above 620. Meanwhile, although a greater proportion of Affirm’s consumer base has higher FICO ratings, we strive to responsibly extend access to credit to as many people as possible and we view consumers as more than just their credit scores alone. This shows up in our underwriting.

The real story on default rates

One of the most significant findings from the CFPB's report is that BNPL default rates are substantially lower than credit cards: “BNPL borrowers defaulted on 2% of their BNPL loans. In comparison, BNPL borrowers defaulted on 10 percent of the credit cards they held during the same time period.”

The report suggested the difference might be attributed to automatic repayment requirements of many BNPL platforms. Yet, the authors do very little to substantiate that conclusion. And that reasoning significantly oversimplifies the story.

Dramatically lower default rates for Affirm’s financial products, as compared to credit cards, are driven by several major advantages - that are both structural and the result of significant investment.

Core to that is our sophisticated underwriting model, which evaluates each transaction individually before making a real-time credit decision. We stand out by offering transparent financing options with no compound interest, late fees, or hidden charges. This transaction-level underwriting approach allows us to responsibly extend credit to more consumers, aligning with CFPB findings that requiring down payments and offering lower credit amounts than sought by the consumer increased approval rates for BNPL loans.

Because we have zero business benefit to extending access to credit that is not repaid, we only approve consumers for what we believe they are able to repay – thereby creating an environment where consumers are better positioned to succeed.

In short, our success depends on consumers’ successfully managing their finances. Revolving lines of credit are the antithesis to this approach as the lender’s interest may not always be aligned with the borrower.

Credit cards: the trillion-dollar elephant in the room

What's notably absent from the CFPB's latest analysis is more context around the massive burden on American households from traditional credit cards – one of the largest sources of non-housing debt for most U.S. consumers.

Earlier research from the CFPB highlighted 'that BNPL imposes significantly lower direct financial costs on consumers than legacy credit products.' In that research, the CFPB found that consumers pay more than $14 billion annually in credit card late fees alone – which they identified as "the most significant fee assessed to cardholders in both dollar amount and frequency." Affirm, for our part, has helped consumers save $316 million in late fees through our no-late-fees posture.

But the CFPB’s newest report acknowledges it didn't analyze whether credit card balances were being revolved – meaning cardholders are paying compounding interest on their purchases. This is a critical distinction and a big omission as the majority of U.S. households revolve on a credit card, with the average household carrying over $7,000 in revolving credit card debt, to the tune of $1.1 trillion in 2023. This is another major structural difference between Affirm and credit cards.

Credit cards enable consumers to borrow from a revolving line of credit. As long as consumers make at least the minimum payment each month (which nearly 30% do), they are able to keep spending against the line of credit until they’re maxed out. If the consumer pays off their balance in full, they aren’t charged interest. This works great for many but the reality is that the majority of U.S. households “revolve” and carry a balance from one month to the next. In doing so, they rack up interest on all outstanding transactions. The system is designed this way as credit card issuers primarily earn profits from consumers that carry balances, and not from those who pay off their bills in full each month.

A better way forward

At Affirm, we've intentionally designed our products to prevent the debt traps that plague traditional credit cards. Our customers cannot "revolve" their balances – there's no compounding interest, and we succeed when consumers pay down their balances. The average outstanding balance per Affirm user is approximately $660, more than ten times less than the typical credit card debt burden.

The CFPB report raises important questions about industry practices, while also validating key benefits of Affirm’s business model.

As we look ahead, we'll continue working with regulators like the CFPB and industry partners to promote best practices that put consumers first. An essential part of this process is engaging in constructive dialogue that captures all the relevant nuance and context.