By Libor Michalek, President, Affirm

Affirm was founded more than 13 years ago with the mission of delivering honest financial products that improve lives. From day one, we committed to never charge a penny in late or hidden fees. We did this to align our incentives with consumers and because we believe it’s critical to show the true costs of credit at checkout. It’s also just the right thing to do. Upholding this promise requires that we excel at underwriting, and we’ve done just that.

You don’t have to take our word for it: Affirm’s delinquency rates are consistently three-to-four times lower than traditional credit cards (based on data from the Federal Reserve Bank of New York). These results are directly tied to our ability to underwrite every transaction and make the best credit decision at the moment of purchase. Our proprietary technology powering these decisions is also driving a feedback loop that incorporates new data into future models. This ensures our results continue to improve over time, making our performance today stronger than when we started and positioning us for continued strength well into the future.

How does Affirm approach underwriting?

Underwriting is how financial institutions evaluate risk, assess creditworthiness for consumers, and determine eligibility for loans. With traditional credit cards, consumers are typically underwritten for a single, static line of credit, at the point of application, which they then borrow against every time they use the card.

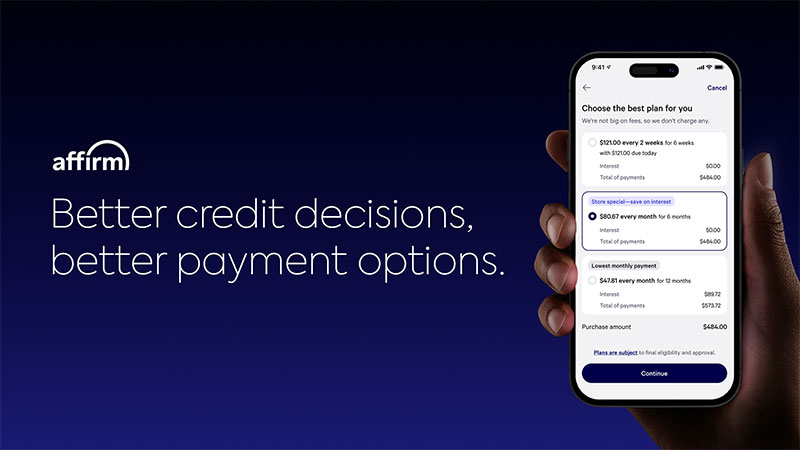

Affirm takes a fundamentally different approach by underwriting each transaction, meaning that every purchase through Affirm is individually evaluated. This enables us to leverage an up-to-date understanding of a consumer’s financial situation, along with context about the purchase they are making. Through this process, we determine the likelihood of a consumer repaying us, and we make a real-time credit decision of whether to approve them and under which terms. In our view, this is a much smarter, easier to understand, and more responsible way to offer credit.

When the consumer selects Affirm as their payment option at checkout, our distinct approach to decision-making begins. It feels simple and instantaneous for the consumer, but behind the scenes, our proprietary technology and machine learning (ML) models are calculating unique-to-Affirm risk scores for the transaction. These risk scores, along with other factors, are ingested into our underwriting engine to make a real-time credit decision and determine the personalized payment plans Affirm is able to offer, with our bank partners. Simultaneously, we are assessing the transaction’s fraud risk, with an intent to keep our consumers safe.

For our credit decisions, we take into account three overarching categories of data:

- External data from credit reporting agencies

- Internal Affirm data, including the consumer’s repayment history and the number of loans they currently have open with Affirm

- Transaction details, including considerations like the requested purchase amount

The risk is assessed for that specific consumer, for that specific transaction, at that specific merchant, and at that specific moment in time. In other words, it's dynamic, not static.

What makes Affirm’s underwriting special?

Through our granular approach to underwriting, our ML models are constantly learning from previous decisions and getting smarter with each new piece of data. We have over 13 years of experience underwriting more than 50 million people for over $100 billion in loans. This combination of history and scale has made us really good at predicting repayment behaviors for consumers across the credit spectrum.

Additionally, our extensive experience underwriting higher-cost purchases has allowed us to develop significantly more sophisticated risk models. Affirm began by underwriting purchases like furniture and exercise equipment with repayment periods lasting up to several years. This taught our underwriting models how to effectively manage the increased risk associated with larger balances paid off over extended timeframes. Since then, we’ve expanded into everyday purchases, and our models now excel at accurately assessing risk across a broad range of transaction sizes – from routine smaller transactions to substantial, highly-considered purchases.

Our underwriting experience also allows Affirm to deliver more customized payment plans compared to traditional BNPL products. Our underwriting engine is not just spitting out one-size-fits-all Pay-in-4 plans. Instead, we’re offering tailored options spanning everything from 30 days to 60 months, for purchases up to $30,000, while maintaining disciplined credit policies, including those of our bank partners. Additionally, we leverage our underwriting capabilities to make more complex credit decisions beyond “yes” or “no” through our personalized payment terms and by sometimes giving consumers the option to make a down payment. This results in more approvals and more purchasing power for our consumers, plus more growth opportunities for our merchants.

The final critical component of Affirm's underwriting are the people who continually incorporate feedback from the current underwriting models into the next version, which is always under development. Affirm handles all aspects of underwriting in-house, unlike other pay-later players who outsource underwriting. We built our proprietary models from the ground up, and have a team of ML and credit engineers who are constantly monitoring and fine-tuning our credit strategies around the clock. Our diligent approach enables our technology to get better and our credit decisions to get smarter, making our underwriting engine truly unique and unlike any other.

Affirm’s approach to underwriting sets us apart from traditional lenders and other pay-later providers, but most importantly it is how we’re able to deliver the most value to our consumers, merchants, and capital partners. Underwriting is the heart of what we do because it enables us to align with consumers’ interests while providing merchants the most dynamic capabilities to fuel their own growth.